29.04.2026

Benefits of EUDI: Why Should You Care About Your Digital Identity

The European Digital Identity Wallet is about to change how you prove who you are — online and offline, at home and across borders. Whether you’re a citizen looking for simpler ways to access services or a business preparing for new compliance requirements, the EUDI Wallet will reshape digital interactions across the European Union. Here’s what you need to know.

The European Digital Identity Wallet is about to change how you prove who you are: online and offline, at home and across borders. Whether you’re a citizen looking for simpler ways to access services or a business preparing for new compliance requirements, the EUDI Wallet will reshape digital interactions across the European Union. Here’s what you need to know.

Why the EUDI Wallet Matters to You in 2026–2030

The European Digital Identity Wallet, or EUDI Wallet, is rolling out across all EU member states by the end of 2026. By November 2027, regulated sectors including banking, telecom, insurance, and energy must accept it for digital identification, making it the new baseline for identity verification across Europe.

So how does this change everyday life? The EUDI Wallet transforms how you interact with both public services and private sector services. Opening a bank account in another country, signing a rental contract, or proving your professional qualifications — all become faster and require less paperwork.

Three core benefits for users:

- Strong privacy through selective disclosure: Share only the necessary attributes (like “over 18”) without revealing your full identity data

- Fewer documents and passwords: One personal digital wallet replaces scattered credentials, physical documents, and repeated form-filling

- Trusted cross border recognition: Your digital credentials work seamlessly across all 27+ member states

Why enterprises should pay attention now:

- Compliance deadlines in 2026-2027 require technical and process readiness

- New KYC and AML expectations will favour wallet-based identity verification

- Early adopters gain competitive advantage through smoother customer onboarding

- Reduced fraud risk from cryptographically signed, tamper-proof credentials

This represents a fundamental shift in how identity verification works. Organisations that prepare now – by integrating EUDI-ready verification flows – will lead in both compliance and customer experience.

What Is EUDI and How Does It Relate to Your Digital Identity?

The EUDI Wallet is formally defined in Regulation (EU) 2024/1183, known as eIDAS 2.0, adopted on 20 May 2024. This digital identity regulation builds on the original eIDAS framework and mandates that each EU Member State must provide at least one wallet to citizens and residents by the end of 2026.

Key terminology explained simply:

| Term | What It Means |

|---|---|

| EUDI Wallet | Your personal digital wallet for storing and sharing identity credentials |

| Personal Identity Data (PID) | High-assurance digital identity equivalent to physical ID documents |

| Legal Person ID (LPID) | Verified identity for businesses and organisations |

| Qualified Electronic Signatures (QES) | Legally binding electronic signatures valid across the EU |

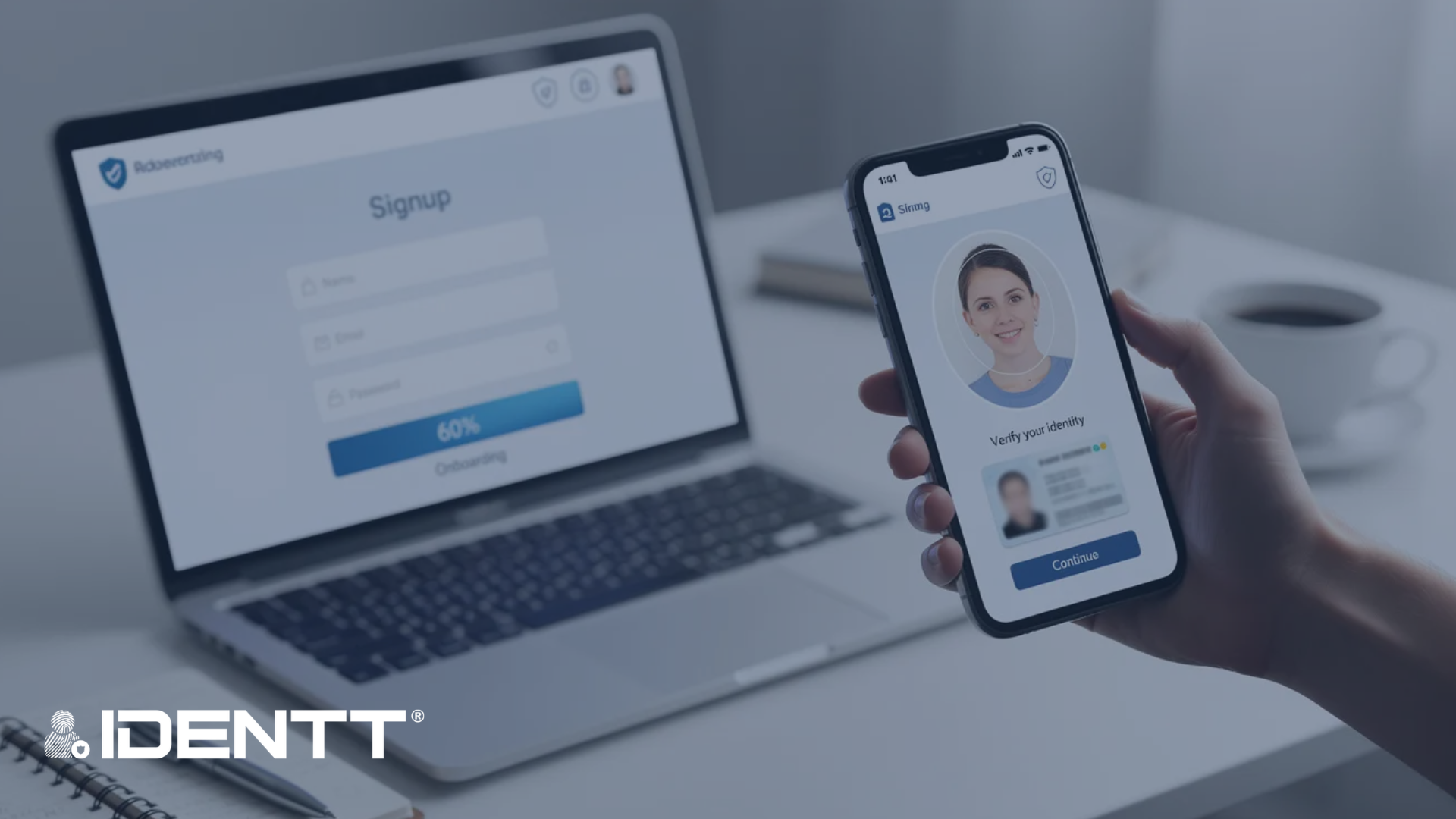

The EUDI Wallet works as a mobile app for individuals and a cloud-based solution for organisations. Critically, this is not a centralised EU database. Your personal data stays under your control, issued by trusted public and private entities, and stored locally on your mobile device or in user-controlled environments.

A practical example: A citizen in Spain wants to open a bank account in Germany entirely online. Using their EUDI Wallet, they share their personal identification data and proof of address credentials directly with the German bank. No scanning documents, no uploading files, no in-person visits. The bank receives verified, cryptographically signed data that meets cross border KYC requirements instantly.

Your Data, Your Rules: Privacy and Control in the EUDI Wallet

User control sits at the heart of the EUDI Wallet design. You decide which attributes are shared, when they’re shared, and with whom. Every data sharing transaction requires explicit consent through clear screens in your wallet app: no silent background transfers.

This is where selective disclosure becomes powerful. Instead of handing over a full identity document scan, you can prove specific facts:

- “I am over 18” without revealing your birthdate or name

- “I am a resident of France” without sharing your full address

- “I hold a valid driving licence” without exposing your licence number

Your data is stored locally on your device or in environments you control. Neither the issuers of your credentials nor the relying parties who verify them can track how you reuse those credentials elsewhere. This “no tracking, no profiling” principle means attributes cannot be silently combined to build hidden profiles about you.

The wallet complies with GDPR, eIDAS 2.0, and national cybersecurity certification schemes. This legal framework ensures that your digital identity remains yours.

How Selective Disclosure Protects You

Consider these real-world scenarios where selective disclosure makes a difference:

Age verification for online gaming: An entertainment platform needs to confirm you’re over 18. With traditional verification, you’d upload an ID showing your name, photo, birthdate, and address. With the EUDI Wallet, you tap approve, and the platform receives only a yes/no confirmation of your age eligibility.

Proof of address for a neobank: Opening an account typically requires utility bills or bank statements. With wallet-based verification, you share only a residency credential: no full bills, no account numbers, no payment history exposed.

Student discount abroad: A Dutch retailer offers student pricing. A French student presents their academic status credential from their wallet. The retailer confirms eligibility without accessing the student’s full educational record, nationality, or other personal data.

This approach benefits both sides. Users maintain complete control over what they reveal. Businesses store less sensitive data, reducing their breach exposure and compliance burden.

How EUDI Will Simplify Everyday Life for Citizens and Residents

One wallet app, recognised across all 27+ EU member states, usable for public and private services — that’s the convenience promise of EUDI. By 2030, the European Commission projects that 80% of EU citizens will use a digital identity wallet for mainstream online services.

The EUDI Wallet is free of charge for non-professional use and interoperable across borders. This means your digital credentials travel with you, recognised from Lisbon to Helsinki.

Common life situations simplified:

- Moving to another EU country: Share verified identity and address credentials with landlords, utilities, and government agencies

- Starting a new job: Present employment eligibility and professional qualifications instantly

- Renting a flat: Provide proof of income and identity without mailing paper documents

- Signing contracts: Use qualified electronic signatures that hold legal validity across the EU

Banks, fintechs, telecoms, and public institutions are preparing to integrate EUDI Wallet verification into their onboarding flows. The result: fewer manual checks, faster approvals, and better customer experiences.

Education and Professional Life

Diplomas, professional licences, and training certificates can be stored as verifiable digital credentials in your EUDI Wallet. This transforms how educational and professional qualifications cross borders.

Example scenarios:

A Polish engineer applies for work in Sweden. Instead of mailing notarised copies of degrees and certifications, a process taking weeks, they share cryptographically signed credentials from their wallet. The Swedish employer receives tamper-proof documentation that they can verify instantly.

A French student enrolls at a Dutch university. Academic transcripts, language certifications, and secondary school diplomas arrive as digital documents the university can trust, eliminating fraud risks from forged PDFs.

Time savings are significant. Fraud drops because credentials come from official documents signed by issuing institutions rather than screenshots or scanned copies.

Payments, Banking, and Financial Services

Banks, fintechs, and payment providers can use the EUDI Wallet for strong customer identification and Strong Customer Authentication under PSD2 and the upcoming PSD3 framework.

Scenario: Opening a bank account or applying for a loan remotely. Using your wallet, you share personal identification data, proof of address, and potentially income credentials. The bank receives verified, structured data that feeds directly into their KYC processes — no document uploads, no video calls, no branch visits required.

Qualified electronic signatures from the wallet make loan agreements, investment contracts, and other official documents legally binding across the EU. You can sign documents with the same legal validity as a handwritten signature, processed entirely online.

Travel and Mobility

Mobile driving licences conforming to ISO 18013-7 and other travel credentials feature prominently in large scale pilot projects across Europe.

Practical examples:

A German citizen rents a car in Italy using a mobile driving licence from their EUDI Wallet. The rental agency receives confirmation of driving entitlement through selective data sharing — no full ID scan, no photocopies, just the relevant data they need.

At airport security, a digital version of boarding credentials linked to verified identity streamlines the process. Hotels check in guests using wallet authentication, reducing front desk queues and eliminating the need to photograph physical documents.

Travel providers and mobility platforms can integrate wallet based identity verification with existing security and fraud prevention systems.

Benefits of EUDI for Businesses and Regulated Organisations

From November 2027, regulated businesses serving EU clients must accept EUDI Wallets for electronic identification where applicable. This creates both obligation and opportunity.

Key business benefits:

| Benefit | Impact |

|---|---|

| Lower onboarding friction | Customers complete verification in minutes instead of days |

| Consistent cross border KYC | One integration handles national digital identities from all member states |

| Fewer manual document checks | Cryptographically verified credentials replace document review |

| Reduced identity fraud | Tamper-proof, device-bound authentication blocks synthetic identities |

The EUDI Wallet provides a standardised, government-backed identity layer that plugs into existing onboarding journeys via APIs and SDKs. Early adopters can redesign flows to be “wallet first,” reducing drop-off and improving conversion rates.

Stronger Security and Reduced Fraud Risk

The EUDI Wallet incorporates multi-factor authentication through biometrics and PINs, cryptographic signatures, and device binding. These technical specifications provide higher assurance than simple ID uploads or password-based verification.

How security improves:

- Credentials are cryptographically signed by trusted issuers—tampering is detectable

- Device binding means credentials cannot be easily copied or transferred to attackers

- Selective disclosure reduces the data exposed in any single transaction

- High Level of Assurance (LoA “High” under eIDAS) enables sensitive electronic transactions

Businesses can layer additional risk-based checks on top of wallet authentication: device fingerprinting, liveness detection for biometric data, face matching, and transaction monitoring. Identity theft becomes significantly harder when credentials are bound to specific devices and protected by multiple authentication factors.

Streamlined Cross Border KYC and AML Compliance

Today, KYC across the EU often means reconciling different national ID documents, navigating local regulations, and managing translation of official documents. This creates friction and cost, particularly for private companies operating across multiple markets.

The EUDI Wallet harmonises this landscape. A bank in Portugal can accept a wallet credential issued in Estonia with the same confidence as a domestic ID. The underlying european digital identity framework ensures mutual recognition and consistent assurance levels.

Supporting AML and KYC obligations:

- Verified personal data arrives in structured, machine-readable format

- Proof of address credentials eliminate utility bill reviews

- Professional role credentials support Ultimate Beneficial Owner checks

- All data sharing is logged for audit trails

Operational Savings and Better Customer Experience

Manual document review, back-and-forth email requests, and in-person verification visits consume significant operational resources. Wallet-based verification cuts these costs dramatically.

Example: A fintech that previously took hours or days to verify customers across multiple EU countries can approve most low-risk profiles in minutes using EUDI plus automated checks. The reduction in manual intervention translates directly to cost savings and faster time-to-revenue.

Experience benefits for customers:

- Fewer steps in onboarding flows

- No scanning or uploading of physical documents

- Immediate reuse of credentials for additional products or services

- Consistent experience across different private sector services

The Legal and Technical Backbone: eIDAS 2.0 and EU Standards

eIDAS 2.0 (Regulation (EU) 2024/1183) serves as the updated european digital identity framework for electronic identification and trust services. It builds on the original eIDAS Regulation (EU) 910/2014 and creates the legal foundation for EUDI Wallets across the European Union.

Key regulatory requirements:

- All member states must offer at least one wallet by end of 2026

- Common rules govern trust services, certification, and interoperability

- Large scale pilots running through 2025–2026 validate technical approaches

- Implementing acts detail specific technical specifications and certification requirements

Technical specifications are coordinated through the Architecture and Reference Framework (ARF). Wallets must comply with strict security certifications overseen by national cybersecurity authorities. The EUDI wallet reference implementation provides a common baseline for Member State deployments.

Standards Enabling Secure and Interoperable Wallets

| Standard | Purpose |

|---|---|

| SD-JWT verifiable credentials | Secure, privacy-preserving credential format enabling selective disclosure |

| ISO 18013-7 | Mobile driving licences specification |

| W3C Verifiable Credentials | Interoperable credential data model |

| OpenID Connect | Authentication protocol for wallet interactions |

These standards enable secure issuance, storage, and presentation of identity data across different wallet apps and member states. A credential issued in Spain works in Finland because both systems speak the same technical language.

For enterprises, common standards reduce vendor lock-in risk. Instead of building separate integrations for each national wallet, organisations can support multiple national wallets via a single integration layer.

How Organisations Can Prepare: From Pilots to Full-Scale Adoption

The timeline is clear: legal framework effective from May 2024, large scale pilots running through 2025–2026, full wallet rollout by end of 2026, and mandatory acceptance for many regulated sectors by November 2027.

Practical preparation steps:

- Technical readiness: Review APIs, identity providers, and integration capabilities

- Process redesign: Map onboarding, signing, and support processes to wallet-based flows

- Compliance review: Update GDPR, eIDAS, and sector-specific regulatory documentation

- Parallel preparation: Test EUDI flows while maintaining traditional verification methods

- Limited pilots: Start with specific products, customer segments, or countries

Government agencies and regulated enterprises should begin now rather than waiting for final deadlines. Early movers will refine their approaches while capacity for implementation support remains available.

Integration Strategy and System Readiness

Start by auditing your existing identity verification stack:

- What’s handled in-house versus by third-party providers?

- Which APIs exist for identity data ingestion?

- Which customer journeys are most critical to wallet-enable first?

Define how the EUDI Wallet fits your architecture:

- Primary method: New customers verify via wallet first

- Alternative option: Wallet alongside manual document upload

- Step-up authentication: Wallet for high-risk transactions or elevated privileges

Sandbox and pilot environments are essential for testing wallet flows, error handling, and fallback options. Consider what happens when a user’s wallet authentication fails or when they don’t have a wallet yet.

Compliance, Governance, and Staff Training

Governance tasks require attention before rollout:

- Update KYC and AML policies to reference EUDI credentials explicitly

- Define acceptable assurance levels for different transaction types

- Update records retention policies for wallet-derived data

- Document how wallet verification maps to existing regulatory obligations

Early dialogue with regulators and supervisors confirms how EUDI data satisfies customer due diligence requirements. Don’t wait for formal guidance, engage proactively.

Staff training priorities:

- How to explain EUDI to customers unfamiliar with the wallet

- How to handle wallet-based errors and fallback scenarios

- How to interpret wallet verification results in operational workflows

Conclusions

The EU Digital Identity Wallet (EUDI Wallet) is set to transform how over 450 million Europeans prove who they are — online and offline, across all 27+ member states. Mandated by eIDAS 2.0 (Regulation EU 2024/1183), every EU country must provide at least one certified wallet by end of 2026, with regulated sectors such as banking, telecoms, and insurance required to accept it from November 2027.

At its core, EUDI Wallet gives users control: selective disclosure means you can prove you are over 18 without revealing your name, or confirm your address without sharing a full utility bill. Credentials are stored locally on your device, cryptographically signed, and GDPR-compliant — no centralised EU database, no silent profiling.

For businesses, the wallet removes onboarding friction, harmonises cross-border KYC, and reduces identity fraud through device-bound authentication and tamper-proof credentials. For citizens, it means one app replacing scattered documents — valid from Lisbon to Helsinki.

In Poland, EUDI Wallet will be integrated into the mObywatel app in a pilot launch in December 2026. Activating it will require a one-time strong authentication using an electronic ID card (e-dowód). Polish pilots are already underway as part of the EU-wide APTITUDE and POTENTIAL projects.

The window for preparation is closing. Organisations that build EUDI-ready verification flows now will lead in both compliance and customer experience when the deadlines arrive.

Need a custom solution? We’re ready for it.

IDENTT specializes in crafting customized KYC solutions to perfectly match your unique requirements. Get the precise level of verification and compliance you need to enhance security and streamline your onboarding process.